प्रधान मुख्य आयकर आयुक्त /Principal Chief Commissioner Of Income Tax पूर्वोत्तर क्षेत्र गुवाहाटी /North East Region Guwahati

Events

Date: 05/06/2025

Some moments from the Plantation cum Awareness Drive on Plastic Pollution organised by the O/o the PCCIT, NER, Guwahati at the Bengali Higher Secondary School, Paltan Bazar, Guwahati on 05/06/2025, on the occasion of World Environment Day, 2025.

Date: 07/03/2025

Meeting with stakeholders on the new Income Tax Bill was held at Aayakar Bhawan, Agartala on 07.03.2025. Which was presided over by respected Pr.CCIT, NER Shri Nav Ratan Soni and attended by the members of Tax bar association, CAs, Tax practitioners and Tax payers.

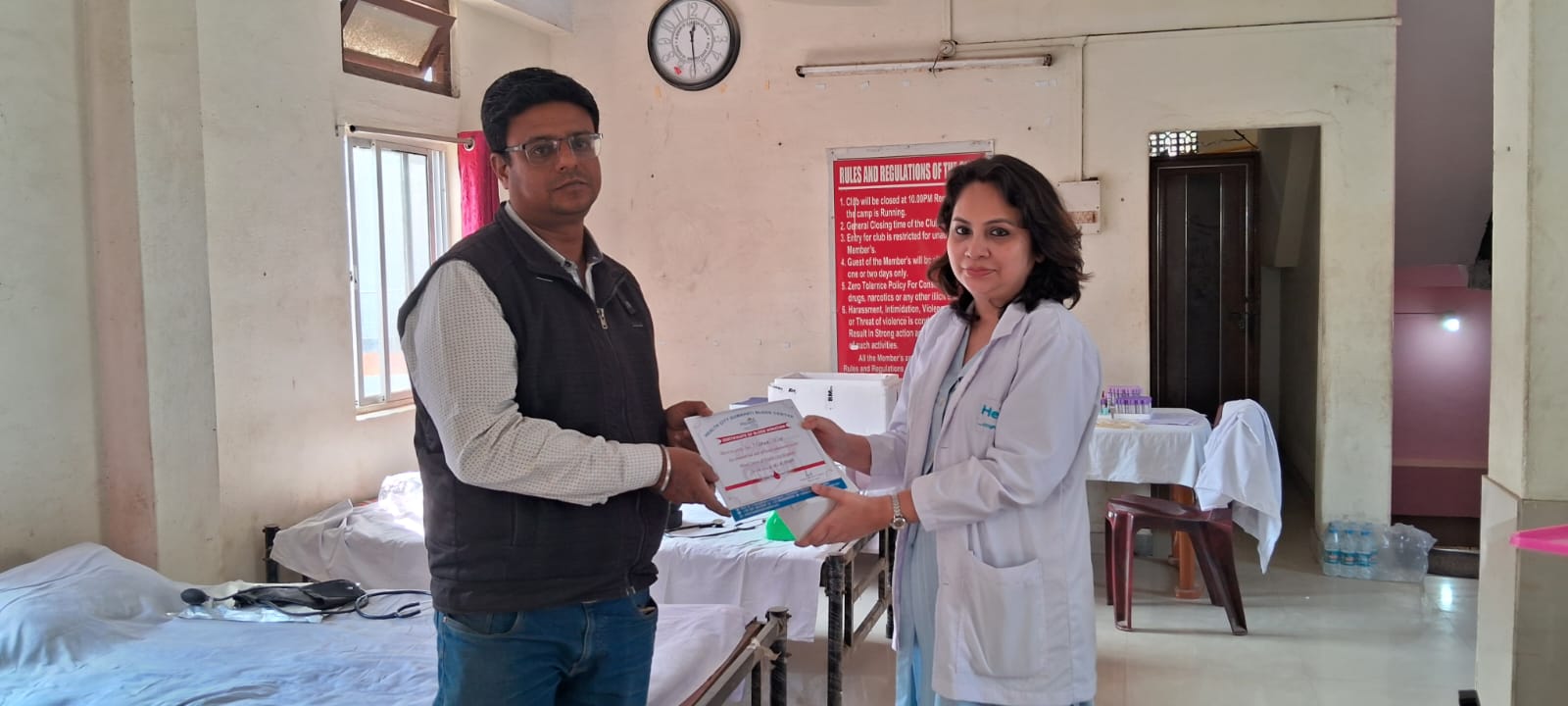

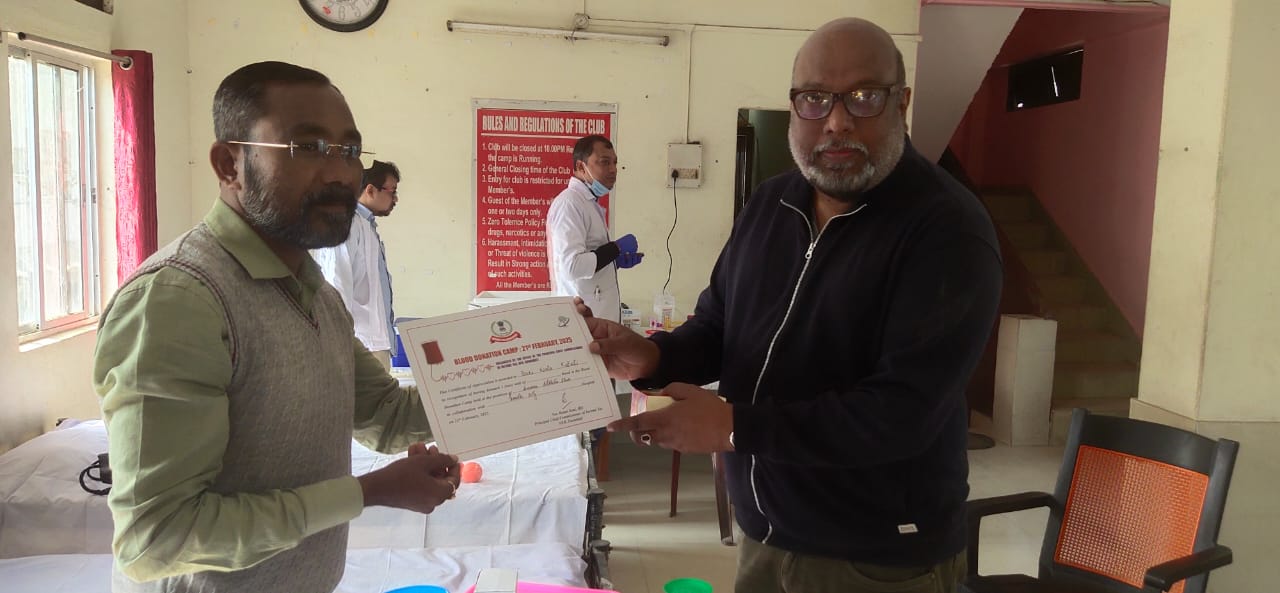

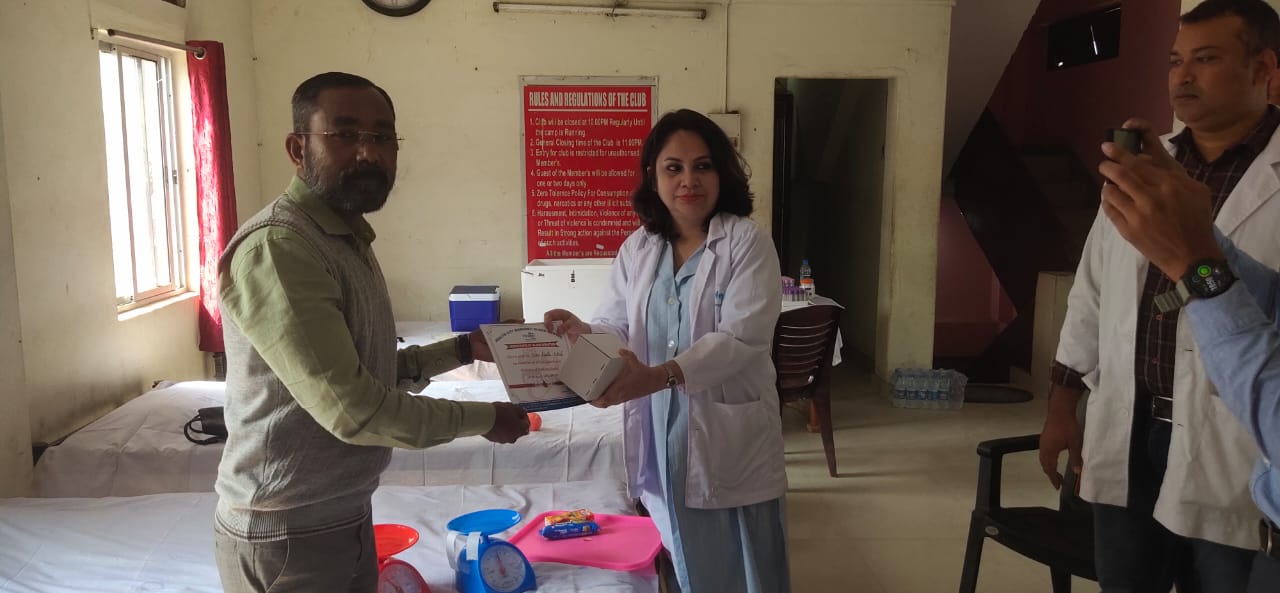

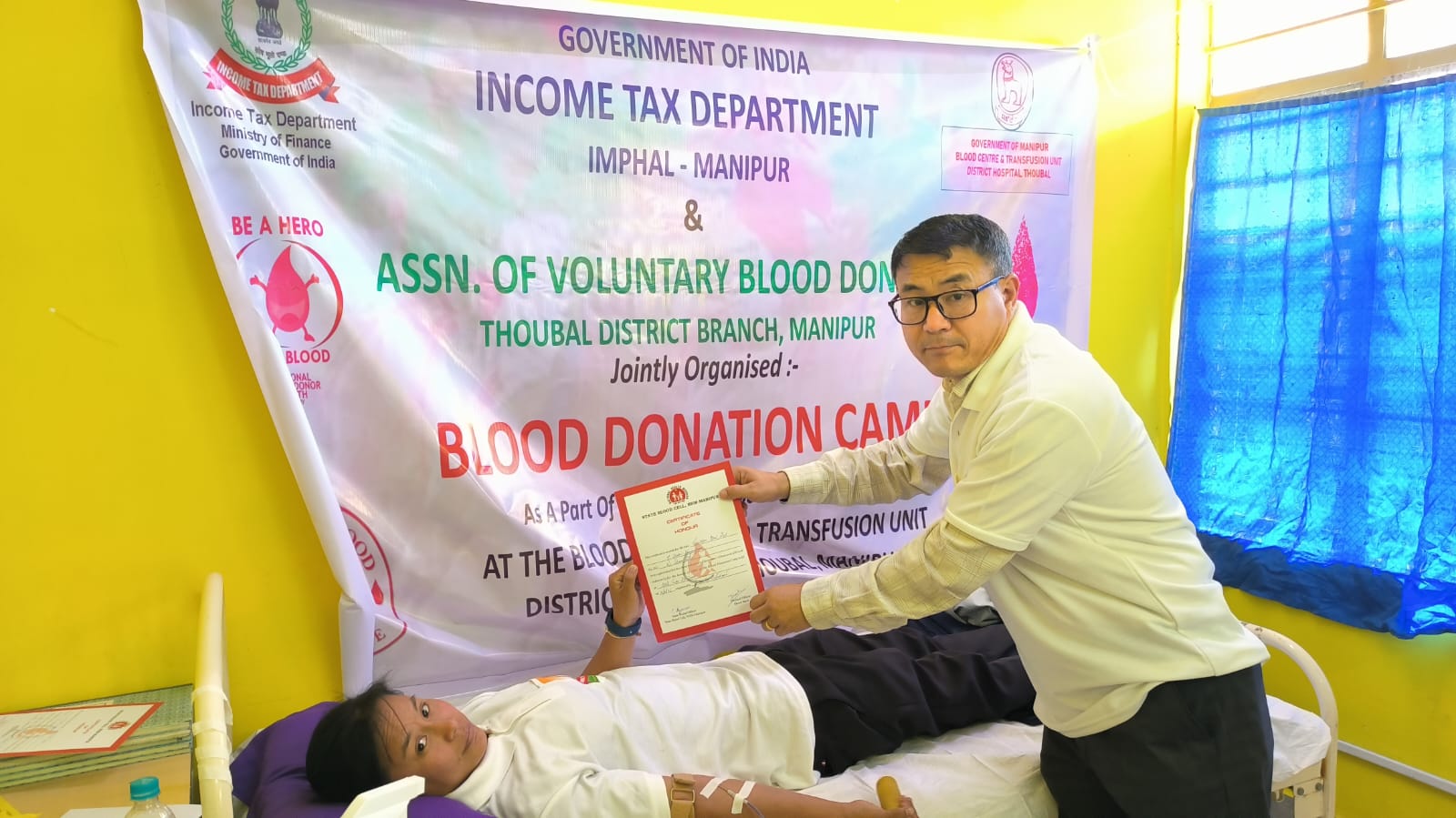

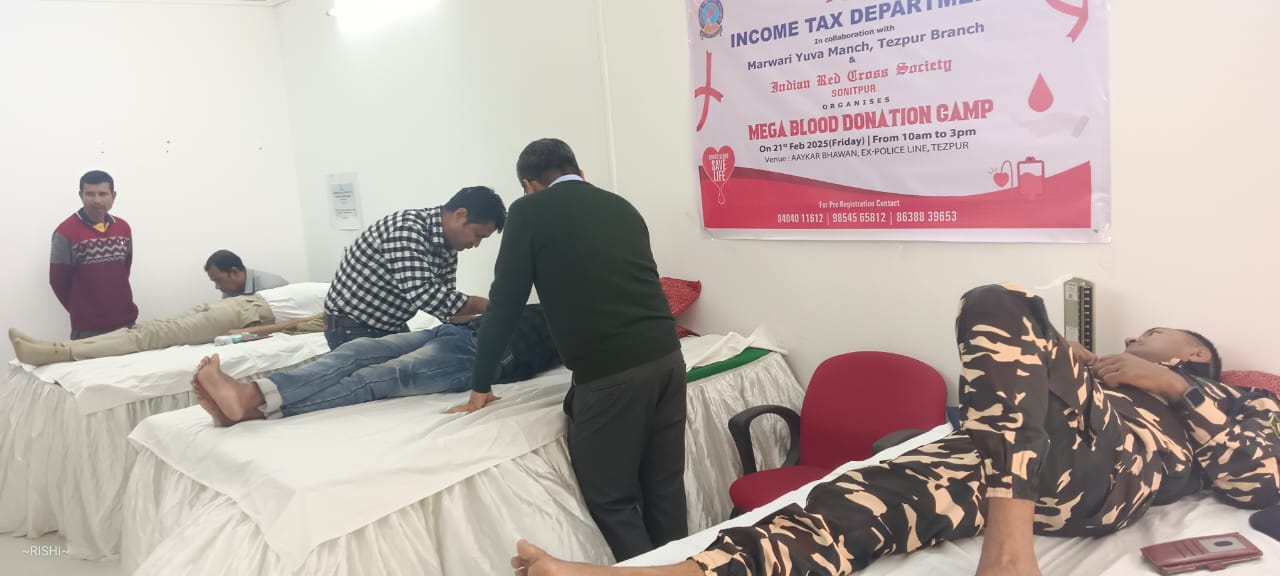

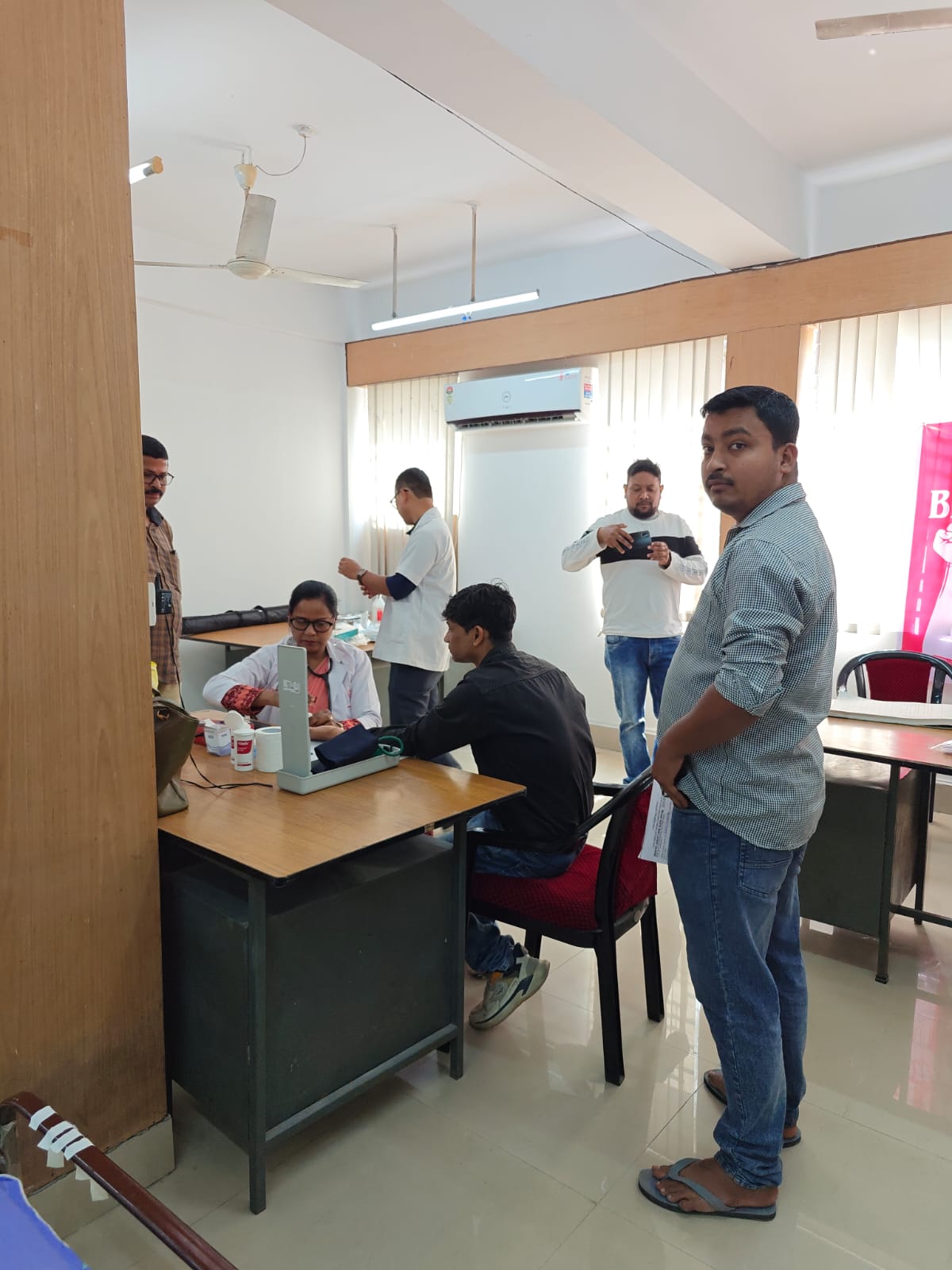

Date: 21/02/2025

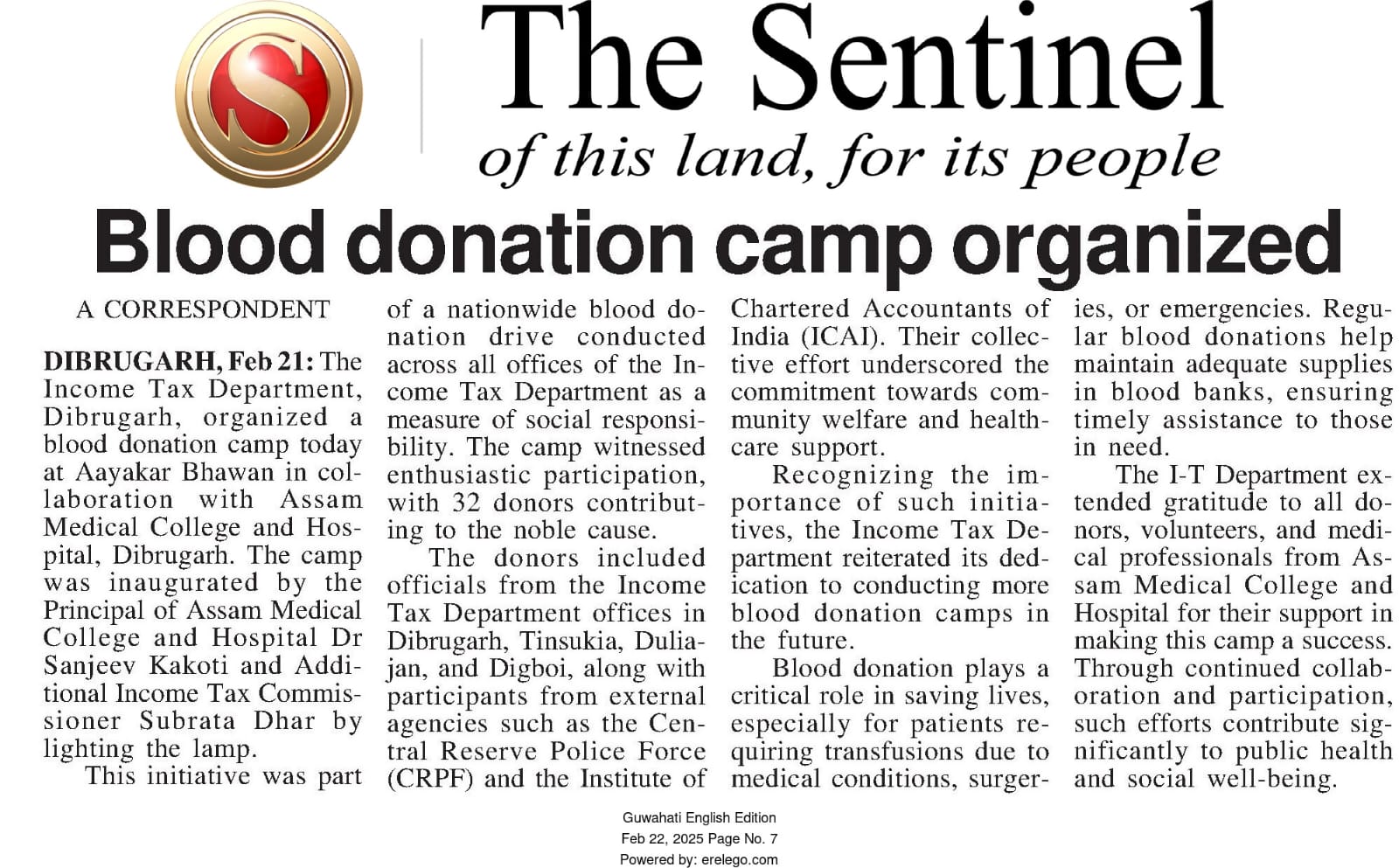

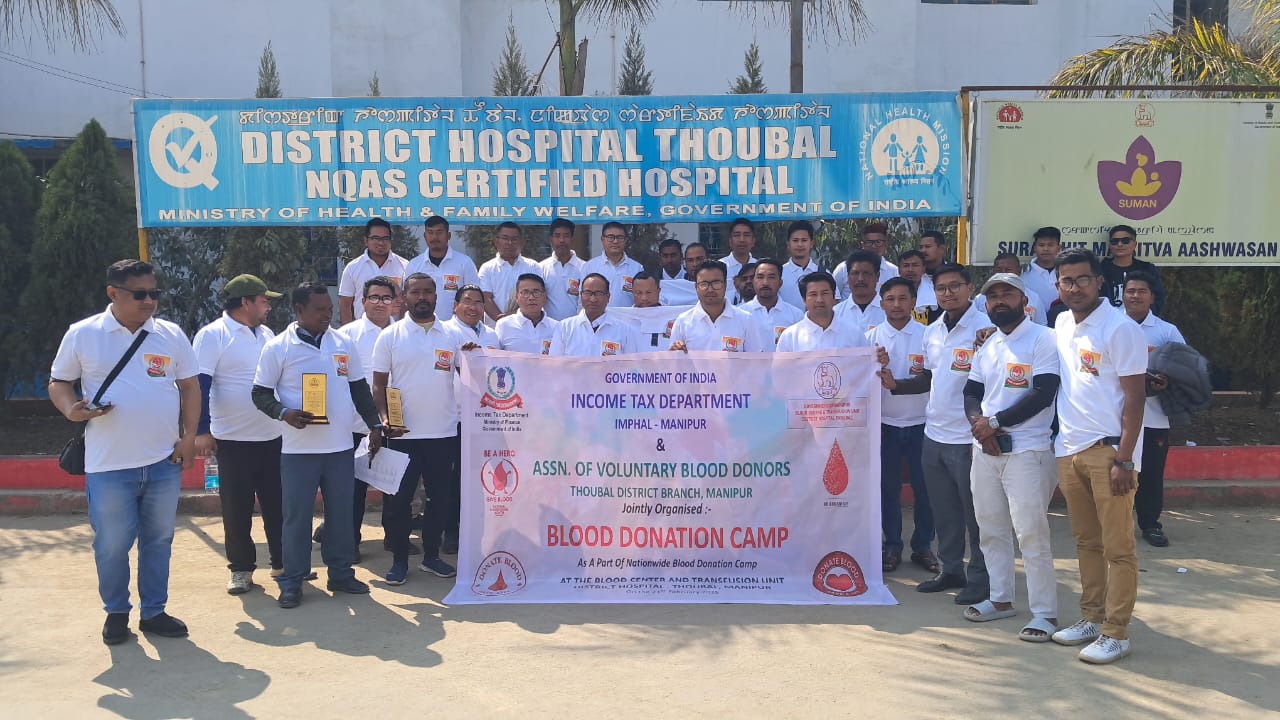

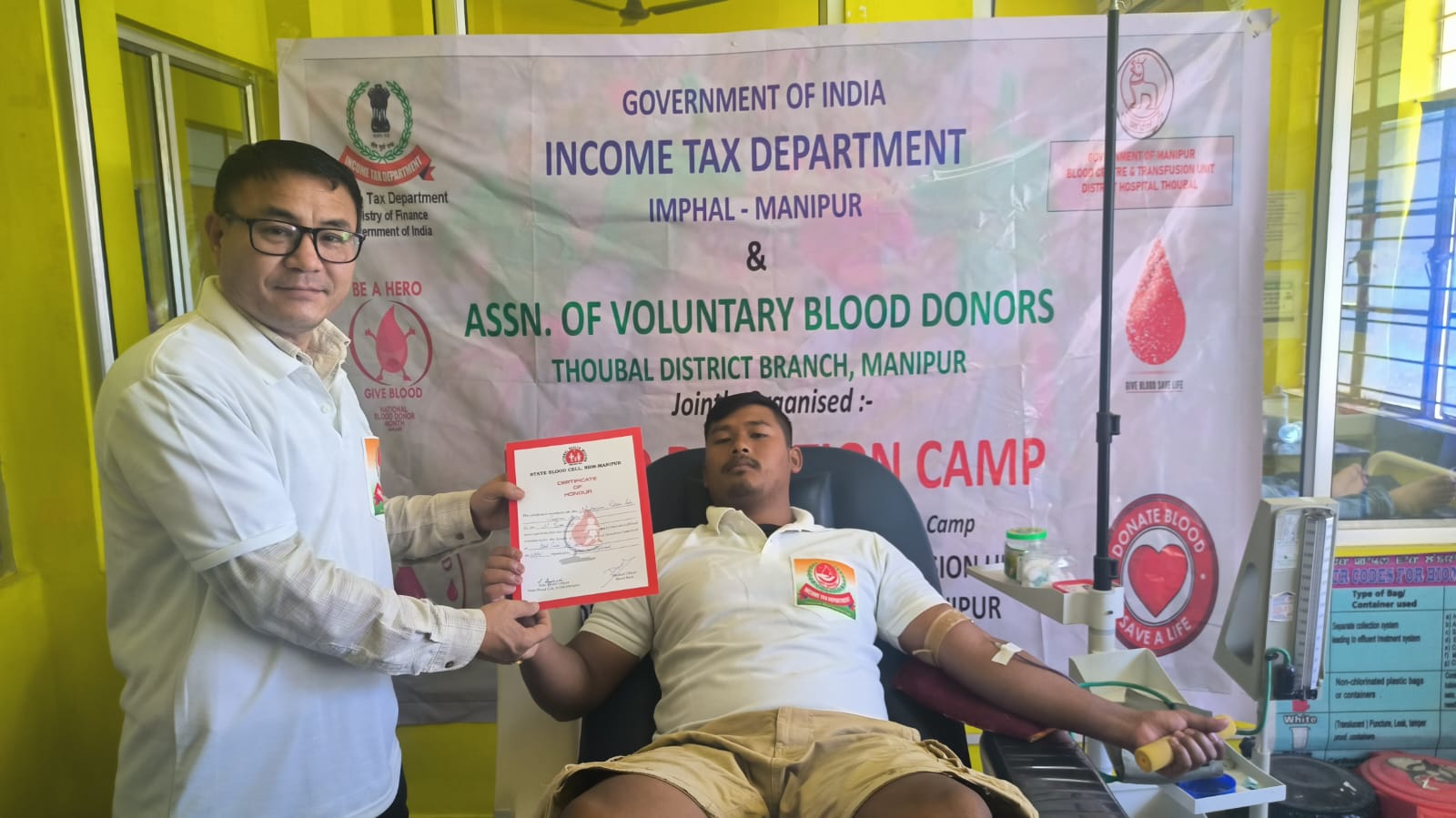

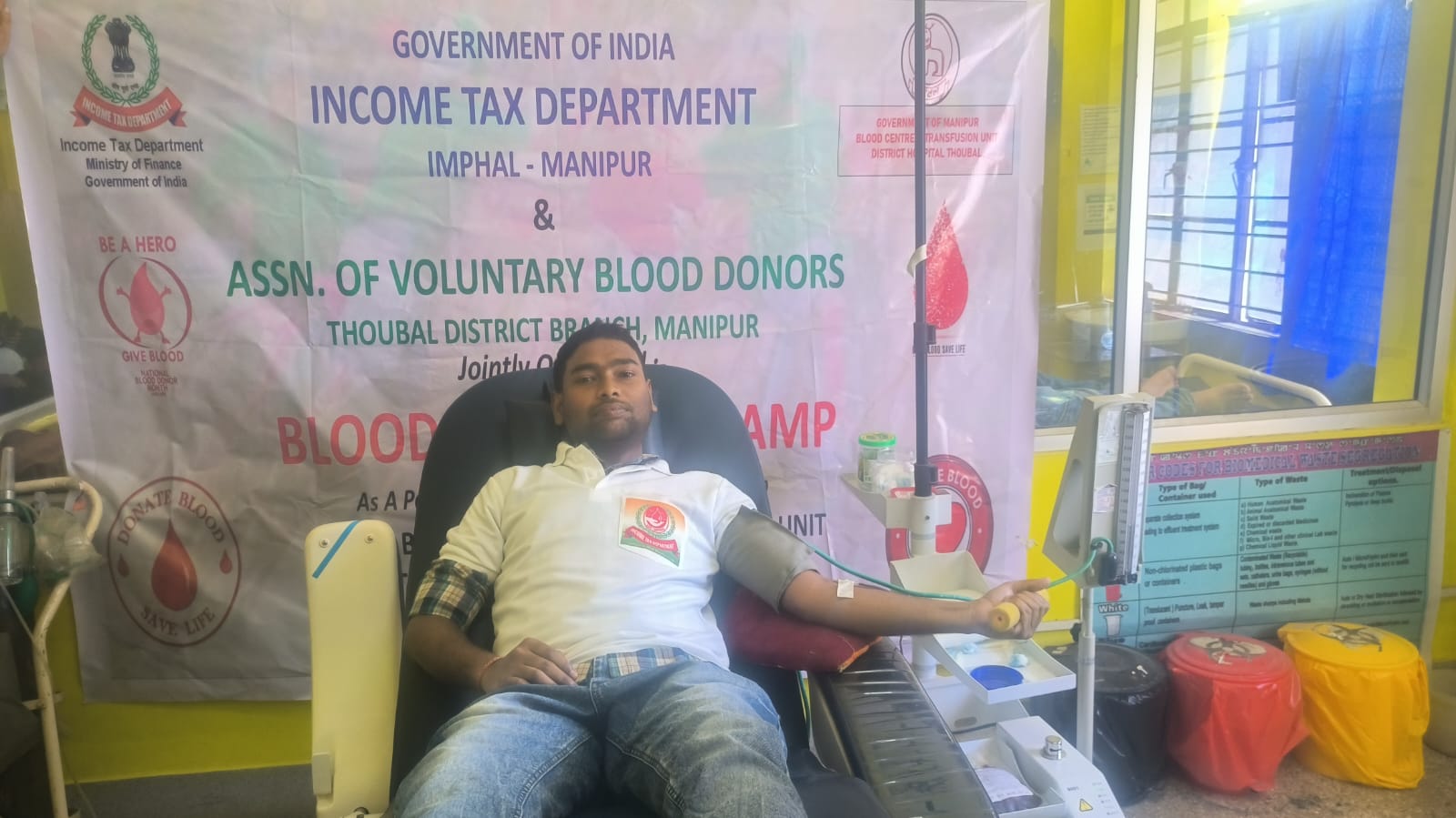

Office of PrCCIT, NER organized Blood Donation Camps at 21 locations today, collecting 534 units from 569 donors. A big thank you to Para-Military units, Educational Institutions, NGOs & Hospitals for their unwavering support.Together, we save lives.

Date: 13/02/2025

A Corporate Connect program on TDS/ TCS compliance was organised by O/o CIT (TDS) NER at Guwahati and graced by the Pr. CCIT, NER Shri Nav Ratan Soni, IRS. More than 100 participants from various stakeholders joined the program. Few glimpses of the event.

Date: 31/01/2025

An outreach program with the students of JNV, Anino, Arunachal Pradesh was organized by O/O Pr. CCIT, NER. Various topics with the future taxpayers of the Nation were discussed with the students. Shri N. R. Soni, Pr. CCIT, NER graced the occasion.

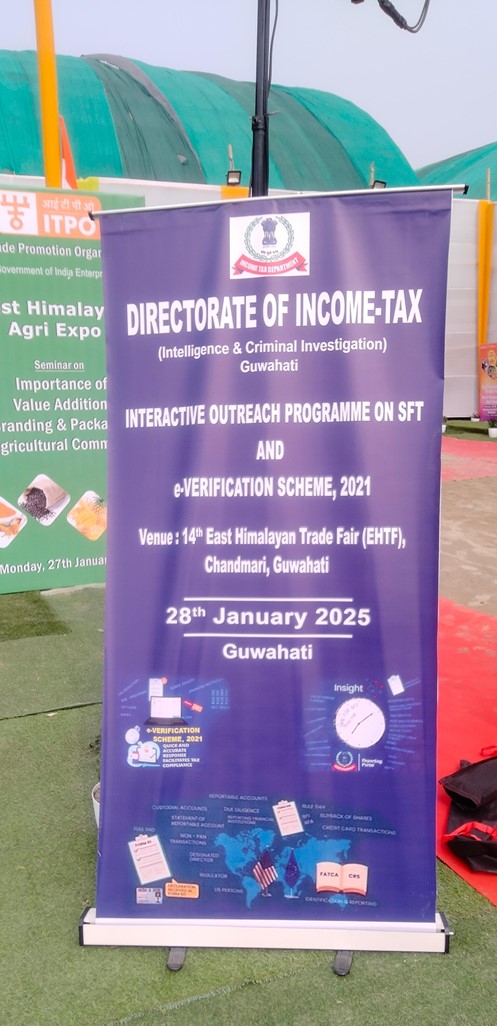

Date: 29/01/2025

Quiz and painting competitions were organized by O/o Pr.CCIT, NER today at 14th East Himalayan Trade Fair,2025, Guwahati. Students from 8 schools participated in the competitions. The event was graced by Shri D.K.Sonowal, IRS, Pr.CIT, Guwahati.

Date:- 28/01/2025

An interactive outreach programme on DTVsVS, 2024 and fraudulent claim of refund was organized at Silchar today in which CCIT, Shillong Smt.N.Longvah, IRS has chaired.

Date:28/01/2025

An outreach programme was conducted by O/o DIT(I&CI), Guwahati today with more than 50 representatives of Co-operative Societies, Co-operative Banks, trade bodies and members of ICAI, Guwahati at 14th East Himalayan Trade Fair 2025

Date:- 27/01/2025

An Outreach programme was conducted by O/o Pr.CIT, Guwahati today at East Himalayan Trade Fair 2025. It highlighted significance of filling ITR, advises against bogus deduction and was attended by MSME representatives and salaried individuals.

Date: 26/01/2025

Outreach programmes on ITR filing and TDS provisions were conducted today at EHTF-25, Guwahati, by the O/o Pr. CCIT, Guwahati, and O/o CIT(TDS). The sessions saw participation from over 100 students, officials, and professional.

Date:26/01/2025

Shri N.R. Soni, IRS, Principal Chief Commissioner of Income Tax, NER, unfurled the National Flag today to mark the 76th Republic Day. The celebration featured cultural programs highlighting patriotism and unity.

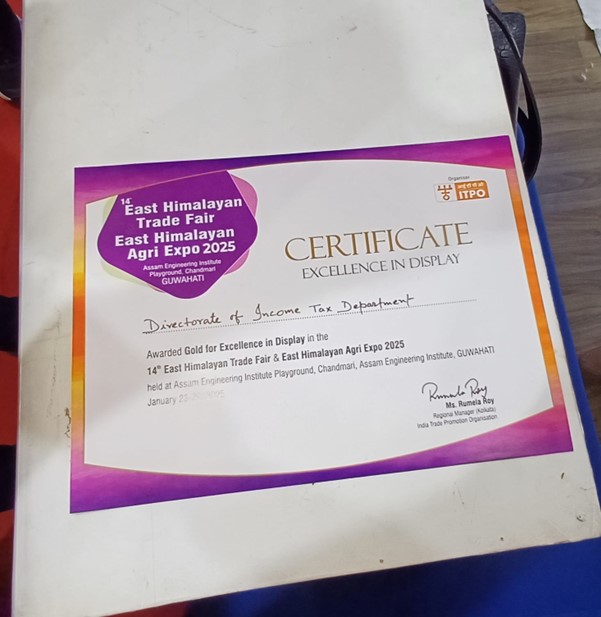

Date:25/01/2025

The Income Tax Department won Gold Medal for Excellence in Display at the 14th East Himalayan Trade Fair 2025, Guwahati. The department rendered various tax payer services through its Taxpayers’ Lounge and outreach seminars from January 23-29, 2025.

Date:-24/01/2025

The Income Tax Department conducted an outreach program today for college students, the future taxpayers of our nation, at the 14th East Himalayan Trade Fair, Guwahati. Talks on income tax, PAN, and engaging activities like quizzes and Nukkad Nataks highlighted the role of income tax in nation-building.

Date: 23/01/2025

A Taxpayers’ Lounge has been inaugurated today by Shri Nav Ratan Soni, Pr. CCIT, NER at the 14th East Himalayan Trade Fair, Guwahati. This initiative will facilitate grievance redressal, outreach to taxpayers, engagement with various stakeholders etc